Introduction

- Convex optimization: Optimizes convex functions over convex sets for guaranteed global solutions.

- Key concepts: Convex sets, functions, and optimality conditions ensure efficient algorithms.

- Applications: Critical in machine learning, control systems, and engineering design.

- Objective: This lecture explores convexity, conditions, and practical implications.

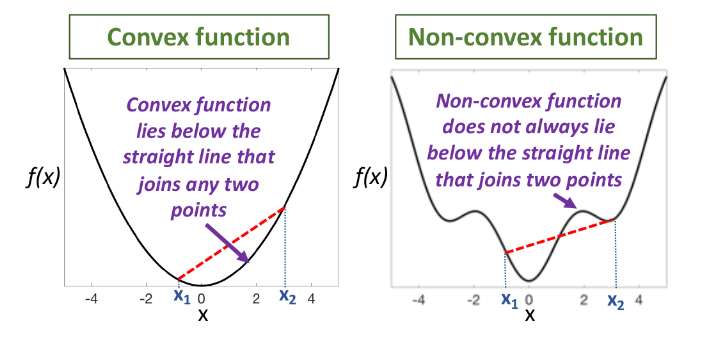

What is Convexity?

Convex Set

A set \( C \subseteq \mathbb{R}^n \) is convex if for any \( \mathbf{x}, \mathbf{y} \in C \), the line segment joining them lies in \( C \):

\[ \theta \mathbf{x} + (1-\theta) \mathbf{y} \in C \quad \forall \theta \in [0,1]. \]

Convex Function

A function \( f: C \to \mathbb{R} \) is convex if for all \( x, y \in C \) and \( \theta \in [0,1] \):

\[ f(\theta x + (1 - \theta)y) \leq \theta f(x) + (1 - \theta)f(y) \]

- Strictly convex: Inequality strict (\( < \)) for \( x \neq y \).

- Concave: \( -f \) is convex.

Why Study Convex Optimization?

- Global Optimality: Any local minimum is a global minimum.

- Efficient Algorithms: Solvable in polynomial time.

- Theory: KKT conditions are sufficient.

Key Insight: Convexity eliminates bad local minima, simplifying optimization.

Applications

- Linear/Quadratic Programming: Optimizing linear or quadratic objectives.

- Machine Learning: SVMs, regression models.

- Control Systems: Signal processing and design.

How to Test for Convexity?

First-Order Condition (Differentiable \( f \))

\( f \) is convex if:

\[ f(\mathbf{y}) \geq f(\mathbf{x}) + \nabla f(\mathbf{x})^T (\mathbf{y} - \mathbf{x}) \quad \forall \mathbf{x}, \mathbf{y} \in C. \]

(Function lies above its tangent hyperplane.)

Second-Order Condition (Twice Differentiable \( f \))

\( f \) is convex if its Hessian is positive semidefinite:

\[ \nabla^2 f(x) \succeq 0 \quad \forall x \in C. \]

For scalar functions: \( f''(x) \geq 0 \).

Example

- Scalar: \( f(x) = x^2 \), \( f''(x) = 2 > 0 \), convex.

- Multivariable: \( f(x,y) = x^2 + xy + y^2 \), Hessian \( \begin{pmatrix} 2 & 1 \\ 1 & 2 \end{pmatrix} \), eigenvalues \( 1, 3 \geq 0 \), convex.

Convex Optimization Problems

Standard Form

\[ \begin{aligned} \text{Minimize} \quad & f(\mathbf{x}) \\ \text{subject to} \quad & g_i(\mathbf{x}) \leq 0 \quad \text{(convex constraints)} \\ & h_j(\mathbf{x}) = 0 \quad \text{(affine constraints)}, \end{aligned} \]

where \( f \) and \( g_i \) are convex, \( h_j \) are affine.

Examples

- Linear Programming: \( f(\mathbf{x}) = \mathbf{c}^T \mathbf{x} \), \( g_i(\mathbf{x}) = \mathbf{a}_i^T \mathbf{x} - b_i \).

- Quadratic Programming: \( f(\mathbf{x}) = \frac{1}{2} \mathbf{x}^T Q \mathbf{x} + \mathbf{c}^T \mathbf{x} \), \( Q \succeq 0 \).

Non-Example

\( f(x) = x^3 \): Not convex (Hessian \( 6x \) not always \( \geq 0 \)).

Optimality Conditions

Theorem: Global Optimality

For convex \( f \), any \( \mathbf{x}^* \) with \( \nabla f(\mathbf{x}^*) = \mathbf{0} \) is a global minimum.

KKT for Convex Problems

- Necessary and Sufficient: If \( f \), \( g_i \) convex, \( h_j \) affine, and Slater’s condition holds, KKT conditions ensure optimality.

- No Duality Gap: Strong duality holds.

Slater’s Condition

Exists a strictly feasible point: \( g_i(\mathbf{x}) < 0 \) for all inequality constraints.

Practical Implications

- Reliability: Convex problems have tractable solutions.

- Algorithm Choice: Gradient descent, Newton’s method, interior-point methods with guaranteed convergence.

- Reformulation: Non-convex problems approximated as convex (e.g., relaxations in integer programming).

- Limitations: Not all problems are convex, but convexity is powerful when applicable.

Summary

- Convexity: Ensures global optimality and efficient algorithms.

- KKT Conditions: Necessary and sufficient for convex problems.

- Applications: Spans machine learning, engineering, and control systems.

- Next Steps: Explore numerical methods, engineering applications, and machine learning optimization.